CG Wealth Management June Newsletter

Personal Note from the Team

Tax Season

As we close out another tax season, and all do a collective sigh of relief as most of us all no longer need to scramble to collect various tax slips and documents, we wanted to thank you for your time, effort, and cooperation over the past few months!A friendly reminder that if you or your spouse/common-law partner are self-employed, your deadline to file your 2025 taxes is June 15, 2026.

As the weather starts to warm up, we wanted to wish all our farmers a good luck as they begin seeding and hope that this season is a bountiful one.

The team has been hard at work and is excited to share some updates in the near future on some of the projects we have been undertaking.

Enjoy this monthly edition of the CG Wealth Newsletter!

Market Updates

The top headlines in the market in April were:

U.S. Equities Stage a Powerful Rebound: U.S. stock markets delivered one of their strongest monthly performances in years amid a robust Q1 earnings season that was largely overshadowed by ongoing geopolitical tensions. The S&P 500 climbed to new all-time highs near the end of April and closed above 7200.

Canadian Equities Post Solid Gains: The S&P/TSX Composite Index rose above 3.5% in April. Performance was mixed across sectors as Canadian markets benefited from broader global risk appetite and a resilient domestic backdrop.

Oil Prices Remain Volatile Amid Geopolitical Developments: Brent Crude continued to experience swings due to disruptions in the Strait of Hormuz related to the U.S.-Israel-Iran conflict. Prices spiked at times above $100–$110/barrel on supply concerns but eased toward month-end on hopes of diplomatic progress and ceasefire extensions. This volatility weighed on energy stocks while contributing to broader inflation worries.

Precious Metals Pull Back from Earlier Highs: Gold and silver gave up some ground in April after strong gains earlier in the year. Persistent oil-driven inflation concerns and a higher-for-longer interest rate outlook from central banks (including the Fed holding rates) capped upside, even as safe-haven demand remained in the background.

Macro Updates

The top headlines in the macroeconomic sphere in April were:

Central Banks Hold Rates Steady Amid Uncertainty: Both the Bank of Canada and the U.S. Federal Reserve maintained their key policy rates in late April. The Bank of Canada kept its overnight rate at 2.25% on April 29, citing the need to monitor the ongoing Middle East conflict, elevated energy prices, and U.S. trade policy uncertainty. The Bank noted that inflation is expected to rise in the future due to higher oil costs but projected it would ease back toward the 2% target in 2027, assuming oil prices moderate. Similarly, the Federal Reserve in the States held the federal funds rate target range at 3.5%–3.75% on April 29. The decision saw notable dissent, reflecting divided views on balancing inflation risks from the energy shock against growth concerns.

Ongoing Iran Conflict Continues to Disrupt Global Energy Markets and Economic Outlook: The geopolitical tensions stemming from the earlier U.S.-Israel operations in Iran and the partial closure/disruption of the Strait of Hormuz remained a dominant macro factor throughout April. Oil prices stayed volatile and elevated, contributing to higher global inflation pressures. Supply chain strains, higher production costs, and food security concerns (linked to fertilizer and energy prices) are rippling through both advanced and emerging economies.

U.S.-Canada Trade Tensions Persist with Focus on Tariffs and USMCA Review: Trade frictions between the U.S. and Canada continued to weigh on economic sentiment. U.S. tariffs on certain Canadian goods (including steel, aluminum, and autos) remained in place, prompting ongoing negotiations and retaliatory measures. Canadian officials are actively seeking relief ahead of the July 2026 USMCA review. The Bank of Canada highlighted these trade policy uncertainties as a key risk to domestic growth, projecting Canadian GDP growth at a modest 1.2% for 2026.

Learn: What moves a stock’s price?

At its simplest level, a stock price moves because of supply and demand. Think of a stock like a rare collectible or a trendy pair of sneakers: if everyone wants to buy them but only a few people are selling, the price shoots up. Conversely, if a company releases a bad product and everyone tries to sell their shares at once, the price drops to entice a buyer. This constant "tug-of-war" between buyers and sellers is what creates the flickering numbers you see on financial news sites.

Beyond basic trading, the biggest driver of demand is future expectations. Investors aren't just buying a company for what it did yesterday; they are betting on what it will earn tomorrow. If a company reports "strong earnings" (making more profit than expected), investors flock to it like a restaurant that just received a glowing review. If the company hints at trouble ahead, investors might head for the exits. Essentially, the stock price is a "scoreboard" reflecting how much confidence the public has in that company’s future success.

Finally, external forces act like the "weather" for the entire market. Even if a specific company is doing well, macroeconomic factors—like rising interest rates or changes in the global economy—can push prices down. Think of it like a rising or falling tide: when the economic "water" is high and interest rates are low, most boats (stocks) float upward together. When the tide goes out due to inflation or recession fears, even the best companies might see their stock prices dip temporarily as the entire market cools off.

CG Wealth Management April Newsletter

Personal Note from the Team

Tax Season

As we close out another tax season, and all do a collective sigh of relief as most of us all no longer need to scramble to collect various tax slips and documents, we wanted to thank you for your time, effort, and cooperation over the past few months!A friendly reminder that if you or your spouse/common-law partner are self-employed, your deadline to file your 2025 taxes is June 15, 2026.

As the weather starts to warm up, we wanted to wish all our farmers a good luck as they begin seeding and hope that this season is a bountiful one.

The team has been hard at work and is excited to share some updates in the near future on some of the projects we have been undertaking.

Enjoy this monthly edition of the CG Wealth Newsletter!

Market Updates

The top headlines in the market in April were:

U.S. Equities Stage a Powerful Rebound: U.S. stock markets delivered one of their strongest monthly performances in years amid a robust Q1 earnings season that was largely overshadowed by ongoing geopolitical tensions. The S&P 500 climbed to new all-time highs near the end of April and closed above 7200.

Canadian Equities Post Solid Gains: The S&P/TSX Composite Index rose above 3.5% in April. Performance was mixed across sectors as Canadian markets benefited from broader global risk appetite and a resilient domestic backdrop.

Oil Prices Remain Volatile Amid Geopolitical Developments:Brent Crude continued to experience swings due to disruptions in the Strait of Hormuz related to the U.S.-Israel-Iran conflict. Prices spiked at times above $100–$110/barrel on supply concerns but eased toward month-end on hopes of diplomatic progress and ceasefire extensions. This volatility weighed on energy stocks while contributing to broader inflation worries.

Precious Metals Pull Back from Earlier Highs: Gold and silver gave up some ground in April after strong gains earlier in the year. Persistent oil-driven inflation concerns and a higher-for-longer interest rate outlook from central banks (including the Fed holding rates) capped upside, even as safe-haven demand remained in the background.

Macro Updates

The top headlines in the macroeconomic sphere in April were:

Central Banks Hold Rates Steady Amid Uncertainty: Both the Bank of Canada and the U.S. Federal Reserve maintained their key policy rates in late April. The Bank of Canada kept its overnight rate at 2.25% on April 29, citing the need to monitor the ongoing Middle East conflict, elevated energy prices, and U.S. trade policy uncertainty. The Bank noted that inflation is expected to rise in the future due to higher oil costs but projected it would ease back toward the 2% target in 2027, assuming oil prices moderate. Similarly, the Federal Reserve in the States held the federal funds rate target range at 3.5%–3.75% on April 29. The decision saw notable dissent, reflecting divided views on balancing inflation risks from the energy shock against growth concerns.

Ongoing Iran Conflict Continues to Disrupt Global Energy Markets and Economic Outlook: The geopolitical tensions stemming from the earlier U.S.-Israel operations in Iran and the partial closure/disruption of the Strait of Hormuz remained a dominant macro factor throughout April. Oil prices stayed volatile and elevated, contributing to higher global inflation pressures. Supply chain strains, higher production costs, and food security concerns (linked to fertilizer and energy prices) are rippling through both advanced and emerging economies.

U.S.-Canada Trade Tensions Persist with Focus on Tariffs and USMCA Review: Trade frictions between the U.S. and Canada continued to weigh on economic sentiment. U.S. tariffs on certain Canadian goods (including steel, aluminum, and autos) remained in place, prompting ongoing negotiations and retaliatory measures. Canadian officials are actively seeking relief ahead of the July 2026 USMCA review. The Bank of Canada highlighted these trade policy uncertainties as a key risk to domestic growth, projecting Canadian GDP growth at a modest 1.2% for 2026.

Learn: What moves a stock’s price?

At its simplest level, a stock price moves because of supply and demand. Think of a stock like a rare collectible or a trendy pair of sneakers: if everyone wants to buy them but only a few people are selling, the price shoots up. Conversely, if a company releases a bad product and everyone tries to sell their shares at once, the price drops to entice a buyer. This constant "tug-of-war" between buyers and sellers is what creates the flickering numbers you see on financial news sites.

Beyond basic trading, the biggest driver of demand is future expectations. Investors aren't just buying a company for what it did yesterday; they are betting on what it will earn tomorrow. If a company reports "strong earnings" (making more profit than expected), investors flock to it like a restaurant that just received a glowing review. If the company hints at trouble ahead, investors might head for the exits. Essentially, the stock price is a "scoreboard" reflecting how much confidence the public has in that company’s future success.

Finally, external forces act like the "weather" for the entire market. Even if a specific company is doing well, macroeconomic factors—like rising interest rates or changes in the global economy—can push prices down. Think of it like a rising or falling tide: when the economic "water" is high and interest rates are low, most boats (stocks) float upward together. When the tide goes out due to inflation or recession fears, even the best companies might see their stock prices dip temporarily as the entire market cools off.

CG Wealth Management February Newsletter

Personal Note from the Team

Tax Season

As we begin the 2025 tax season, we wanted to remind you of a few key dates to keep in mind:

The deadline to file and pay for any income tax owing for the 2025 tax year is April 30, 2026.

The deadline to file your 2025 taxes if you (or your spouse/common-law partner) are self-employed is June 15, 2026.

As mentioned before, our firm partners with former CG Wealth Partner, Glen Koshman, who prepares income tax filings on behalf of clients who are interested in utilizing this service.

If you’ve never utilized this tax service before or have not notified us recently that you would like to use this service, please let our team know and we will send you the instructions, detailing the process this year for Glen preparing your income tax return.

Portfolio Adjustments

Since November 2025, we have been executing on structural changes to our portfolios. In summary, across our three portfolio series (Global, Strategic, & SMA), we have been adjusting to be more defensive. In simpler terms, we have been increasing the cash or cash equivalent positions in the portfolios. As well, we have decreased our portfolio’s allocation to the U.S. and have spread that to other markets, like Canada and the cash equivalents.

The reason for these adjustments is that in our view, the market could be due for a correction in the short term. The valuations of companies, especially in the U.S., have started to become overvalued, and as a result, the market in general. Combined with the increased geo-political uncertainty that seems to be the new norm, we feel that these factors could lead to a sell off in the market. While we are not guaranteeing a correction, we have a responsibility to you, the client, to protect your investments. And with these two factors that we see as potential risks, we felt it necessary to adjust the portfolios as such.

Our goals with the restructuring are simple. The first is to lower the potential drawdown on client’s portfolios if we do see a correction. The second is if there is a correction, we have the cash liquidity to inject back into the market when the prices are low, capturing the tailwinds when the market begins to rise again.

If you have any questions about any of these portfolio adjustments, feel free to give the office a call.

What’s New

Chris Earns his Portfolio Management Designation

We are excited to announce that Chris has officially earned his Portfolio Management designation! This prestigious designation not only solidifies his numerous years of experience in the financial industry but also allows him to take on greater responsibilities in discretionary portfolio management, advising on investment strategies, and delivering tailored solutions to clients with enhanced expertise and regulatory recognition. Congratulations to Chris on this well-deserved achievement—we look forward to the continued value he brings to our team and clients!

Aaron Becomes Partner at the Firm

In other exciting news, we are happy to announce that Aaron Hill has officially become a Partner here at CG Wealth Management! Since joining our team in July 2024, Aaron has been diligent in supporting clients’ needs, working to earn various investment licenses and designations, while greatly helping shape and grow the company in various avenues. We look forward to Aaron continuing his education and experience in his current role as an Associate Advisor and now as a Partner.

Market Updates

The top headlines in the market we have been watching are:

Global Oil Prices Surge: Despite the focus of this month’s newsletter on primarily recapping the month of February, we wanted to highlight the surge in oil and the primary factor causing this spike in March. Brent Crude, a global benchmark for oil prices, reached highs in March of nearly $120 USD /barrel. With the States and Israel’s targeted military operations in Iran in early March, Iran has responded by effectively closing the Strait of Hormuz through attacks on commercial vessels, many of which transport oil from the Gulf countries through this strait to around the world. With this restriction on oil supply and no material change on the demand side, the price per barrel has sharply increased as a result.

Gold and Silver surge to new all-time highs: Gold peaked at a record high of approximately $5,600 per ounce while silver reached a record of approximately $120 per ounce before selling off. Various market and macro-economic factors, such as industrial demand, geopolitical shocks, and monetary policy uncertainty, drove commercial and retail investors to continue to buy into the precious metals market, bolstering the high prices experienced in the first of quarter 1.

6 of the 7 US Mega-Cap names reported earnings in January and February:

Macro Economy Updates

The top headlines in the macroeconomic sphere we have been watching are:

Interest Rates held in Canada and the U.S.: Canada and the U.S. both had interest rate announcements during the first quarter of the year and both countries held their key interest rates at their current levels. Canada’s key interest rate is still at 2.25% and the U.S.’ key interest rate is still 3.75%. Both country’s next rate announcement is scheduled for March 18, 2026.

Conflict in Iran Increases: On February 28, 2026, the United States and Israel launched large-scale joint airstrikes (Operation Epic Fury) across Iran, killing their Supreme Leader, Ali Khamenei, and numerous senior officials, while targeting nuclear facilities, missile sites, air defenses, and military infrastructure. Iran retaliated with hundreds of ballistic missiles and drones against Israel, U.S. bases in the region, and allied countries, causing casualties and widespread disruption. While Iran has effectively closed the Strait of Hormuz through direct attacks on commercial vessels, drone and missile strikes, naval mines, and threats from the IRGC, halting most global oil and LNG transit (about 20% of world supply) and driving oil prices to nearly $120 USD/ barrel. Iran's new Supreme Leader, Mojtaba Khamenei, issued his first public statement vowing to keep the strait blocked as a "tool of pressure". The IEA has released massive oil reserves to mitigate the crisis, shipping insurance has been canceled for the route, and global economic ripple effects continue amid calls for regime change from the US and no clear end in sight.

New Canada x China Trade Deal: The governments of Canada and China announced a new trade deal between the two countries. The deal centered around a reciprocal reduction of tariffs on some of the country’s respective industries. Most notably coming out of the deal:

Electric Vehicles: Canada will lower its tariff on Chinese-made Electric Vehicles with the aim for further reductions in tariffs on these Chinese vehicles in future years.

Agricultural Exports: China will significantly slash tariffs on Canadian canola seed by March of 2026.

Thecountries also agreed to reduce tariffs in other areas such as Seafood, crop pulses, steel & aluminium.

CG Wealth Management January Newsletter

Personal Note From Chris Getzlaf

To all our valued clients, we hope you had a great holiday season and a happy New Year! As our physical office was closed over the Christmas season, we have now reopened and are back to regular working hours. As we turn the page on 2025, we wanted to touch on a few points.

TFSA Contribution Limit Increases

The CRA has officially announced the contribution limit increase for Tax-Free Savings Accounts (TFSAs) in 2026. As of January 1, 2026, eligible individuals will gain an additional $7,000 in contribution room.

With this increase, eligible Canadian residents who have never contributed to a TFSA and have been at least 18 years of age since its inception in 2009 will have a total cumulative contribution room of $109,000 as of 2026.

At some point during one of our past meetings, we’ve probably discussed the many benefits of utilizing a TFSA to save and invest your money. Quite frankly, with advantages like tax-free growth on investments within the plan and tax-free withdrawals (including principal and earnings), it remains one of the best ways to build wealth for yourself and your estate.

Our office has already been in touch with many of you about contributing to your TFSA for 2026. However, if this reminder has you thinking about contributing, please feel free to give us a call or send us an email.

Tax Season on the Horizon

With tax season approaching, we wanted to outline some important dates to keep in mind:

The last day to contribute to an RRSP or Spousal RRSP for your 2025 taxes is March 2, 2026.

The deadline to file your 2025 taxes is April 30, 2026.

The deadline to file your 2025 taxes if you (or your spouse/common-law partner) are self-employed is June 15, 2026.

If you’re new to CG Wealth and have never gone through a tax season with us, here’s some information for you. Our firm partners with former CG Wealth Partner, Glen Koshman, who prepares income tax filings on behalf of our clients for those who wish to participate. Typically, we send out a mass communication in February to clients who are on our list who have used this service before, instructing them on where to send their various tax slips. If you’re interested in having Glen prepare your taxes for the 2025 income tax season, please send us an email and we will add you to the list.

2026 Market Commentary

As we step into 2026, it is natural to wonder what the year ahead holds for the markets, economy, and our portfolios. Will interest rates rise or fall? Will inflation persist, or will growth accelerate? What’s the next major geo-political event? Typically In January, major institutions produce forecasts and outlooks on these topics, tempting us to speculate on the unpredictable.

This brings to mind a classic insight from legendary investor Peter Lynch, the former manager of Fidelity’s Magellan Fund, who famously quipped in a 1977 speech “if you spend 14 minutes on a year on economics you’ve wasted 12 minutes.” Lynch’s point was simple and profound: No one can reliably predict the direction of the economy, interest rates, or the stock market. History is filled with recessions, booms, geo-political shocks, and surprises that few-if any forecasters saw coming. Yet, over the long term, quality businesses have continued to grow their earnings, rewarding patient investors who stayed the course.

We start the year with the S&P 500 at 6,908, and TSX Composite at 32,227. There are indicators there is pressures on the global economy between consumer and federal debt, stretched valuation multiples, inflation, and global reserves purchasing record amount of gold; mix in questions surrounding geo-politics, there are signs that a correction could be on the horizon at some point. However. sentiment on the stock market is bullish for 2026 with S&P 500 2026 estimates from the major investment banks ranging from 7,100 to 7,800.

We don’t have a target price for the S&P500 or TSX Composite, nor believe in setting one. We do believe when looking at these general market indicators, there are valid reasons for cautious optimism and are avoiding certain areas of the market. Often, there has been more money lost in waiting or anticipating a market correct than the actual correction. In 1928 the founder of Merrill Lynch (now part of Bank of America), Charles Merrill, warned investors of a bubble; while he was eventually right - the market rose 90% to September 1929 before he was “right.” In October of 1999, if noise was clouding your judgement, you would have watched the market rise 40% higher before correcting. So, the question should become “do I have faith that in 5, 10, 20 or more years public businesses still be the place to invest?” We do, and the philosophy of our SMA portfolios, where we buy quality companies at attractive prices and participate in their future earnings growth, is steadfast. These are businesses with strong fundamentals like wide moats, consistent profitability, predictable cash flows, and strong solid balance sheets.

What makes us cautiously optimistic about the market? In simplest terms, valuations. Operating earnings need to continue to surpass expectations for justifications of current valuations. As can be seen in the chart below, anytime the S&P 500 has purchased at a multiple beyond 22 prices-to-earnings, future expected return of 5% or more years skews; the forward 10-year annualized returned averaged -2% to positive 2%.

Not all companies are trading at extreme valuations. This is where our SMA Portfolios strive to look for companies that we feel are trading at attractive entry valuations. Currently, names outside of the top 10 companies in the S&P 500 are our US focus, in addition, we plan to remain overweight Canada as their companies look cheaper on a relative basis, and we can gain additional exposure to commodity companies that will play a crucial role in the development of technological infrastructure. Our focused thoughts on our SMA Portfolios will be part of a yearly SMA review letter that will be released every June.

CG Wealth Management January Special Edition

As we close out the month September, and quarter 3 (Q3) all together, I hope you were able to enjoy all that summer had to offer. With the official beginning of fall and the restarting of all things busy (work related, family related, school related, etc.) I wanted to quickly touch on the RESP season that we are in.

Personal Note From Chris Getzlaf

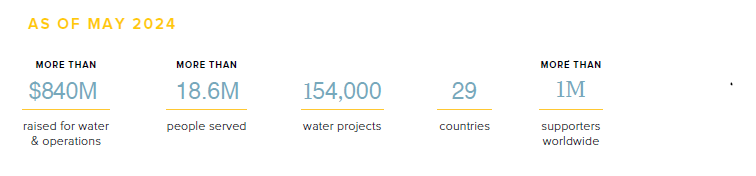

Last year, our team had an opportunity to meet Scott Harrison, founder of Charity: Water, during a conference we were attending. During Scott’s presentation, he discussed his lifelong passion and his mission of bringing clean water to people around the world. His message is incredibly inspiring! His organization allocates 100% of all donations specifically to bringing clean water to the world. We know we can help make a lasting impact on the lives of many. In lieu of any Christmas gifts this year, we have decided to team up with Bluesky in our office and together, build a new clean water well in a community of great need and we are excited to share our progress with all of you after 12 months once we start receiving updates.

Our $10,000 donation will build our own clean water well in a community of need. Imagine, walking miles per day to bring home dirty water for your family to drink, replaced with a tap that brings clean water to your entire community steps away from your home.

There are over 1 billion people on this earth who do not have access to clean water. Charity: Water has helped over 18.6 million people worldwide but there is still a long way to go. 771 million more to go to be more exact!

What sets Charity: Water apart is its radically transparent approach: 100% of public donations go directly to water projects in the field. Every dollar of our holiday donation goes straight to the project itself – not overhead, salaries, or fancy travel or funding a private yacht somewhere.

Imagine walking hours per day to obtain a basic life necessity, water. Now imagine how your life and community would change when you can replace those hours of walking to collect potentially unsafe water with a tap in your neighbourhood that provides, clean, SAFE, drinking water every day.

We heard stories of children enrolling in school, more family members able to earn an income and entire communities being empowered. You can imagine the difference in their lives that clean water provides beyond the health benefits.

Imagine that, a tap, something we generally take for granted will fundamentally change their lives forever.

To learn more about Charity: Water, you can click the link below

CG Wealth Management October Newsletter

Personal Note From Chris Getzlaf

As we close out the month September, and quarter 3 (Q3) all together, I hope you were able to enjoy all that summer had to offer. With the official beginning of fall and the restarting of all things busy (work related, family related, school related, etc.) I wanted to quickly touch on the RESP season that we are in.

RESP Season

We are nearing a month into the new fall semester for university students. If you’re a client who has a Registered Education Savings Plan (RESP) and are planning on making a redemption to pay/help pay for your child/grandchild’s education, what we need to unlock monies from the plan is a copy of the student’s proof of enrollment and proof of pay for the fall semester.

If you’re reading this, have a child or grandchild who is not yet in post-secondary education, they will likely attend in the future years, and you’re wanting to help them pay for their educational costs, a RESP could be for you! Some key information about this type of plan are:

-It is a government-registered plan, whose goals is to help individuals save for their children/grandchildren’s post-secondary education.

-You can invest the money within a RESP, like how one would with a TFSA or RRSP.

-When to deposit money into the plan, you receive a government grant (the Canadian Education Savings Grant – CESG) of 20% on contributions up to $2,500 per year per child. Low-income individuals may be eligible to receive additional government funding when they contribute to the plan through the Canada Learning Bond (CLB).

-Investments grow within the RESP tax-deferred until they’re withdrawn. When a withdrawal occurs, typically any government grant received and any interest earned on investment is taxable to the beneficiary, aka the student. However, the student will likely have low to no taxable income as they’re in school, so taxes owed from the withdrawal could be low to nil. Not to mention that with school comes the potential to claim expenses that could further reduce any potential taxes owed.

-You can contribute to a RESP with a regular deposit schedule or through lump sum deposits throughout the year.

If you’re interested in learning more about RESPs and if they would be right for you, send me an email and I would be happy to discuss.

Send your questions about RESPs!

-Chris Getzlaf, Partner at CG Wealth Management

Market Updates

The top headlines in the market in April were:

Markets Continue to Rally:

The S&P/TSX Composite Index, Canada's stock market benchmark, delivered strong results in September 2025, rising approximately 4.92% for the month and contributing to a robust Q3 overall. The index gained over 11% in Q3 (12.5% including dividends), outperforming the U.S. S&P 500's 7.8% (8.1% total return) for the quarter. This performance defied seasonal weakness and broader economic headwinds. Year-to-date through September, the S&P/TSX Index is up over 20% reflecting resilience amid global uncertainties.

Small Caps and Value Outperform Large-Cap Growth in Q3:

In Q3, we broadly saw sector rotation occur within the market as the Russell 2000 (a U.S. index that measures the performance of 2,000 small-cap companies within the U.S.) outperformed the S&P 500 (which tracks the performance of the top 500 companies in the U.S. – like Apple, Google, Meta, etc.). During this timeframe, the Russell returned over 14% whereas the S&P returned 9%.

US Government Increases Deals and Equity Stakes with Local Companies:

The U.S. government significantly expanded its engagement with private companies through a mix of traditional contracts and innovative equity investments. This shift aimed to bolster strategic sectors like semiconductors, critical minerals, AI, energy, and defense. Some of examples of these deals can be found below by clicking on the title

Macroeconomic Updates

The top headlines in the macroeconomic sphere in April were:

Interest Rates Cut in Q3:

In Q3, the Bank of Canada (BoC) held two interest rate announcements (July 30 and September 17) and one monetary policy report. On July 30, the BoC held the overnight interest rate at 2.75%, citing high economic uncertainty from tariff fueled global trade as the primary reason for the unchanged rate. On September 17, the Bank of Canada (BoC) lowered its overnight rate by 0.25% to 2.5% - its first cut since March - citing tariff-induced damage to growth and employment, alongside cooling inflation at 1.9%.

Canadian Unemployment Rate Surges to 7.1%:

August's labor data, released early September, revealed a net loss of 66,000 job and pushed the unemployment rate to 7.1%, a nine-year high outside the COVID period. Manufacturing, transportation, warehousing, and professional services led in the greatest decreases in employment.

Inflation Eases to 1.9%, but Tariff Risks Loom for Price Pressures:

August’s inflation data, released in mid-September, showcased a 1.9% increase in The Consumer Price Index (CPI), year-over-year. Prices at the pump contributed the most to the acceleration in the all-items CPI. BoC reports warned that sustained U.S. tariffs could reignite inflation via higher import costs.

Learn: The Power of Life Insurance

Debt is a part of life for many of us—whether it’s a mortgage for your dream home, a car loan, or credit card balances from unexpected expenses. But what happens to those debts if you pass away unexpectedly? Without a plan, your family could be left struggling with payments, facing financial stress, or even losing assets like your home or car. Life insurance is a simple yet effective way to manage this risk, ensuring your debts don’t become a burden for your loved ones. Life insurance is a powerful tool as it can cover outstanding debts, protect your family’s financial future, and give you peace of mind.

Let’s explore how insurance can help your family, the most common types of policies, and why it’s a smart move for anyone with debt.

How Life Insurance Can Cover Your Debts?

Regardless of the kind of policy you may choose, by matching the policy amount to your debt (e.g., a $250,000 policy for a $250,000 mortgage), you ensure your family isn’t left with unmanageable bills. An additional perk of Life insurance is the flexibility it provides to your beneficiaries. Rather than be forced to use the entire payout from the policy for one specific thing, a person could choose to do what they want to do with the money – clear the debt entirely, keep making regular payments on the debt and invest the policy payout, or a combination of both.

The Kinds of Insurance Policies

Not all life insurance policies are the same. Here’s a simple breakdown of the three most common forms that can help manage your debt:

Term Insurance

What it is: Covers you for a specific period (e.g., 10, 20, or 30 years) and pays a death benefit if you pass away during that time.

Best for: Debt protection on a budget. It’s the most affordable option, ideal for covering temporary debts like a mortgage or car loan.

Example: A 30-year, $200,000 term policy can match your mortgage term, ensuring the home is paid off if you pass away.

Pros: Low premiums, straightforward, and flexible terms.

Cons: No payout if you outlive the term and no cash values are built within the policy.

Whole Life Insurance

What it is: Covers you for your entire life and includes a cash value component that grows over time, which you can borrow against.

Best for: Estate building purposes, long-term financial planning, or if you want a policy that builds savings while covering debts.

Example: The death benefit can pay off debts, and the cash value can be used during your lifetime for emergencies or debt reduction.

Pros: Permanent coverage that builds cash value, has predictable premiums, and beneficiaries receive the payout tax-free

Cons: Higher premiums than a term policy

Universal Life Insurance

What it is: Offers lifelong coverage with flexible premiums and death benefits, plus a cash value that grows based on interest rates.

Best for: Estate building purposes, those who want flexibility to adjust payments or coverage as debts or financial needs change.

Example: Adjust the policy to cover a growing mortgage or reduce coverage after paying off debts.

Pros: Flexible, builds cash value, provides permanent coverage as long as premiums are paid, and beneficiaries receive the payout tax-free

Cons: Premiums can vary, and cash value growth depends on market rates.

Which Policy is Right for You?

While you may be able to see how one of the above policies could be a fit for you and your family, that is where our team comes in. As Chris is licensed broker for Life Insurance, he would be happy to sit down and talk through if a life insurance policy is right for you and which one can most benefit you and your current situation.

CG Wealth Management July Newsletter

The first of many changes to announce is that after a successful and monumental 40-year career within the financial industry,

Personal Note From Chris Getzlaf

As we closed out the month of June, marking the end of quarter two (Q2) and nearing the half way mark of 2025, I wanted to update you all on some exciting work that the team has been undertaking.

New Portfolios

A little over a week ago, CG Wealth has officially launched a Separately Managed Account (SMA) and have developed three new portfolios with the SMA as a major component within each. The three new portfolios are CG Equity SMA, CG Growth SMA, and CG Balanced SMA.

In simple terms, a SMA is a portfolio of individual securities managed by a professional asset manager on behalf of a single investor. The expertise and experience that Braydon brings from his previous background has greatly enabled the firm to build the SMA and begin offering the three new portfolios.

Extensive research and analysis has and will continue to go into the picking of securities that are held within the SMA. Regulatory oversite by our back office and governing body ensures compliance requirements are continuously met and upheld.

We launched the SMA and created the new portfolios because we believe they will provide a competitive rate of return relative to the market and add additional alpha to our clients’ portfolios while reducing overall fees. Discussion with clients who meet the threshold to hold one of the new SMA portfolios will occur as meet throughout the year.

Monthly Statements

A general note to all our clients, that as of August 1st, 2025, IPC (our head office) will begin charging your accounts for paper copies of your monthly statements. For those who have elected to receive electronic copies, there is no cost to you, and nothing will change. For the majority of those who still receive paper copies of your monthly statements, we will be opting you in to receive electronic copies of your monthly statement to avoid any charges to your accounts. At some point within the next month, you can expect us to send you your online login information via DocuSign so that you can access your online statements and view your account values.

Calendly

A note that within the last year, we have began using a new booking software system for client meetings called Calendly. Calendly allows you to look at my schedule and select a time that works for the both of us for a meeting. So, if you receive a Calendly invite from our reception, myself, or one of my assistants, please take a look through available times to book an appointment.

To all our valued clients, I wish you all the best wherever you’re reading this and hope that remainder of July is great for you all. Be sure to take some time and enjoy all that summer has to offer.

-Chris Getzlaf, Partner at CG Wealth Management

Market Updates

The top headlines in the market in April were:

Robust momentum in the U.S., uneven elsewhere: Despite recent volatility in the U.S. markets, the S&P 500 is nearing record highs and U.S. earnings growth expectations remain constructive. Following a roughly 25% surge from its April lows, the S&P 500 notched its best quarter since December 2023.

Canadian Markets Inch Higher Despite US Trade Negotiations: In June, the S&P/TSX was up over 3.7%. This positive month added to the over 9% gain the Canadian market experienced in Q2.

Macroeconomic Updates

The top headlines in the macroeconomic sphere in April were:

12-Day War in the Middle East: On June 13, Israel launched "Operation Rising Lion", which targeted Iran’s nuclear and military sites. In retaliation, Iran launched missile and drone strikes across Israel. On June 22, the U.S. entered the conflict by conducting stealth bomber strikes on the Iranian nuclear facilities of Fordow, Natanz, and Isfahan. Just two days later, the U.S. administration brokered a ceasefire between Israel& Iran. The conflict drove market volatility in Canada and the U.S., with oil prices spiking before stabilizing post-ceasefire.

Canada hosts the G7: The 51st G7 Summit was held in Kananaskis, Alberta, during the middle of June. The focus of conversation between the seven leaders that comprise the G7 (Canada, U.S., Japan, France, UK, Germany, and Italy) were global economic stability, energy security, and international peace.

Interest Rates Hold in Canada & US: in both Canada & U.S., national interest rates were held. In Canada, the interest rate remains at 2.75%, and in the States, 4.50%. The underlying argument for the recent holds by the heads of each nation’s central banks were a combination of global trade negotiations, un-realized tariff impacts, and potential inflation risks as a result of sharp increase in global oil prices because of unrest in the Middle East.

Learn: Compounding, the 8th Wonder of the World

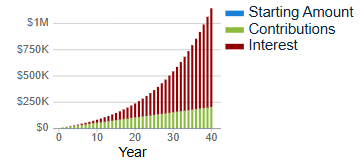

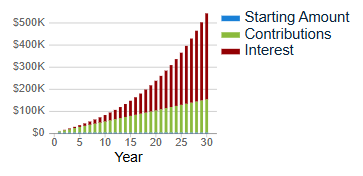

One of the most powerful tools in wealth creation is the concept of compounding. Compounding is the process where investment’s earnings, such as interest, dividends, or capital gains, are reinvested with the original amount you had invested to generate additional earnings over time.

Compounding allows your investments to grow exponentially over time, as your earnings generate additional earnings, creating a snowball effect that can significantly enhance your financial future.

The key to unlocking compounding’s potential is time. Starting early gives your investments more years to grow, amplifying the effect. For example, investing $5,000 annually from age 25 to 65 at a 7% annual rate of return could grow to over $1.1 million by retirement.

Waiting until age 35 to start? That same strategy might yield only $540,000—a difference of over $600,000.

To harness compounding:

Start Early: Even small contributions can grow substantially over decades.

Stay Consistent: Regular investments, even in volatile markets, benefit from dollar-cost averaging.

Reinvest Earnings: Dividends and interest should be reinvested to fuel growth.

Be Patient: Compounding rewards those who stay invested for the long term.

Do you want your money to start compounding? The team is looking forward to helping you plan to prosper.

CG Wealth Management May Newsletter

The first of many changes to announce is that after a successful and monumental 40-year career within the financial industry,

Personal Note From Chris Getzlaf

It has been a little longer than anticipated since the last monthly edition of the newsletter. That delay has been warranted because the office and team have undergone some recent, exciting changes.

The first of many changes to announce is that after a successful and monumental 40-year career within the financial industry, Judi Thiessen, CG Wealth’s longest-serving employee, will be officially retiring from the industry at the end of May. Whether in sports, business, or family, we all know of those one or two persons who are pivotal in helping make the entire thing run, and Judi was one of them for CG Wealth. When Glen and I partnered up in 2018, Judi was on the ground floor. Through her incredible dedication, determination, and client first-focus, she has helped build and establish the firm for what it is today and helped set a successful trajectory for the team. I cannot thank her enough for all her insight, wisdom, and friendship over the years. I am excited for the next chapter she is entering and wish her all the best in her endeavors.

With Judi’s departure, we are excited to announce a few new additions to the team (their full bios can be found at the end of this newsletter). Introducing first, Braydon Tomac. Braydon will eventually be a third advisor on the team and brings valuable institutional knowledge as he has been in the financial industry for over five years and an associate advisor for two of those. Next, Panagiota (Yota) Ntoli Singk, has also recently joined the firm. Panagiota has a background in the financial services sector and brings a plethora of administrative experience that will be greatly utilized well into the future. Last but certainly not least to recently join the team is Erica Burton. Erica too has a well-seasoned administrative background which will support all facets of the company.

Aaron (whom many of you have already met) continues to expand his talents and is still in pursuit of becoming a full-fledge advisor for the firm.

I am very excited for where we currently are as a team, longevity has been established, and everyone brings a unique skill-set that greatly compliments one another.

To all our valued clients, I wish you all the best wherever you’re reading this and hope you have been enjoying spring so far!

-Chris Getzlaf, Partner at CG Wealth Management

Market Updates

The top headlines in the market in April were:

Trump’s “Liberation Day” Tariffs Sparks Global Market Turmoil: On April 2, 2025, President Donald Trump announced sweeping tariffs on what was coined “Liberation Day”. The tariffs included a 10% baseline tariff on all imports (with exceptions), 54% (later raised to 245%) on China, 20% on the EU, and higher rates on countries like Vietnam, Thailand, Japan, Cambodia, and Taiwan. This triggered a sharp sell-off in global stock markets in early April.

Market Rebound After Tariff Pause Announcement: On April 9, a 90-day pause on higher reciprocal tariffs for countries that signaled a willingness to negotiate their current trade practices with the U.S. and on those not yet imposing retaliatory measures. This led to a partial recovery amongst most major financial markets.

Volatility in the Bond Market: U.S. Treasury yields surged after the tariff announcements, with the 10-year yield hitting 4.5% and the 30-year yield jumping over 50 basis points to 4.92% by April 9.

The top headlines in the market in May were:

U.S.-China Trade Truce Sparks Market Rally: On May 12, 2025, the U.S. and China announced a 90-day truce in their trade war, leading to a significant market rebound. Markets were buoyed by optimism for further negotiations, though tensions persisted as China insisted on full U.S. tariff removal before deeper talks.

Corporate Earnings Highlight Resilience: First-quarter S&P 500 earnings showed 73% of companies beating estimates, though slightly below the five-year average.

As this newsletter was being drafted (May 27, 2025), markets have rebounded substantially since the sell off at the beginning of April. Since the April low, the S&P 500 is up over 22%, and is only down around 3% from all time highs back in February. Turning to Canadian markets, the S&P/TSX is up over 13% since the April lows and is currently trading at an all time high.

Macroeconomic Updates

The top headlines in the macroeconomic sphere in April were:

Liberals Win Fourth Consecutive Mandate: The Liberal Party, led by Prime Minister Mark Carney, won their fourth mandate as they formed a minority government on April 28.

Inflation Growth Cooled: According to Statistics Canada, the inflation rate slowed to 2.3% year-over-year, which was largely influenced by lower gasoline and travel tour prices.

Central Bank Holds Interest Rate: Despite the slowed growth in inflation in March, the Bank of Canada held the interest rate at 2.75% on April 16 and did not opt for what would have been an eighth decrease in the interest rate.

The top headlines in the macroeconomic sphere in May were:

Federal Reserve Holds Interest Rate AGAIN: Down in the States, their Central Bank held their key interest rate at 4.50%. This is the third hold in a row for the Central Bank since cutting it’s interest rate last in December 2024.

Inflation Rate Grows Higher than Expected: According to Statistics Canada, the annual inflation rate grew higher than expected at 2.5% year-over-year.

Newest CG Wealth Team Members

With 3 new additions to the team, we have a very capable team to meet your every financial need. Click the link below to get to further know Chris, Aaron, Braydon, Panagiota and Erica!

Please don't hesitate to contact us if you have any questions. The team is looking forward to helping you plan to prosper.

CG Wealth Management April Newsletter

As we are close out on the first quarter of the year, a reminder that (for most) taxes are to be submitted to the CRA by April 30. For those who are waiting to receive your tax slips for your non-registered accounts, investment companies had until the end of March to send them out. For those who are interested in having your tax return completed by Glen Koshman, as noted in the last several editions of this newsletter, please let me know and the team will be happy to send you instructions on when and where to submit your income tax information.

Personal Note From Chris Getzlaf

As we are close out on the first quarter of the year, a reminder that (for most) taxes are to be submitted to the CRA by April 30. For those who are waiting to receive your tax slips for your non-registered accounts, investment companies had until the end of March to send them out. For those who are interested in having your tax return completed by Glen Koshman, as noted in the last several editions of this newsletter, please let me know and the team will be happy to send you instructions on when and where to submit your income tax information.

Turning to the elephant in the room, I want to speak again on the volatility that we are currently experiencing in the market. For those who may not have saw, we had sent out communication earlier this week in response to the market sell-off we saw on Monday. Since then, the market has rallied, sold off, rallied again, and now has had some selling off. My message remains the same, stay patient and we will weather the storm. In times of turmoil, it may be easy to have a knee jerk reaction. I want to challenge those of you who may be feeling uneasy about the volatility we are all experiencing is to try switch to a more longer-term focus. Having a longer-term focus can aide in handling the potential bumpy road to wealth creation.

For those who are invested in our CG Wealth Portfolios, we are actively speaking to our fund managers whose products are apart of our portfolios so that we are up to date on any changes they’re making. In addition to that, we have taken proactive measures to try and help protect against downside risk in the market through diversification. When the portfolios were built, diversification was one of the cornerstones. Diversification in not only the types of equities (stocks) you’re invested in, where the companies operate geographically, the sectors and industries they’re apart of, but also the weightings of asset classes you’re invested in, like equities and fixed income. Building in diversification from the get-go can allow our portfolios to capture the upside in one equity or asset class, when another other is down, thus reducing the overall loss to the portfolio.

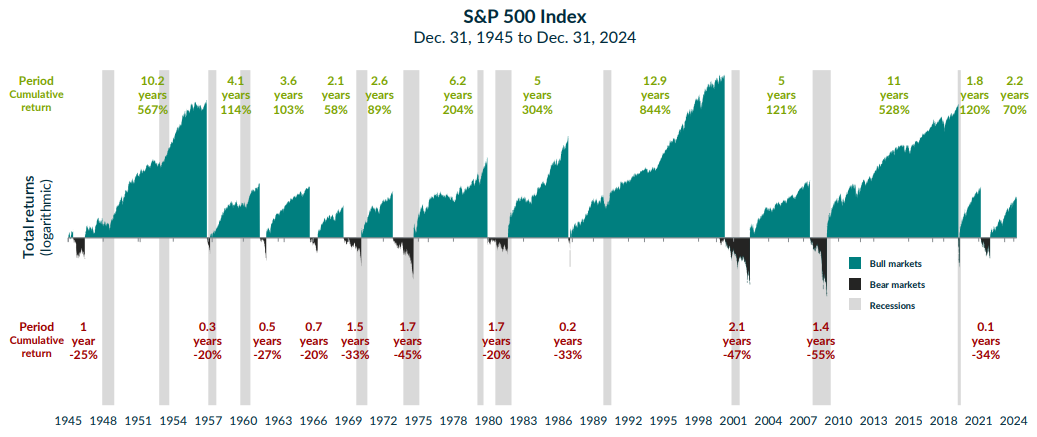

Diversification in investing is one piece of the puzzle. Also remember that it’s about time in the market, not timing the market. When prices in the market are beginning to compress, a natural response can be to sell out of fear because prices could be compressed further. The issue with that mindset is that you could miss out on potential gains. To help further illustrate this point see the chart below.

The chart above shows the performance and length of the S&P 500 Index (one of the major US stock indices) through its bull and bear markets. Although past performance isn’t indicative of future results, looking at historical markets helps illustrate the benefits of investing for the long-term. The average bull market period lasted 5.9 years with an average cumulative total return of 277%. The average bear market period lasted one year with an average cumulative loss of-32%. The S&P has been in a bull market about 86% of the time.

In closing, if after reading all of this and you’re still feeling uneasy about the state of the market, you can always reach out chat with myself. Just give me a call and I would be happy to chat through any concerns you may have.

Enjoy this month’s edition of our newsletter and be sure to take advantage of the sunnier weather that April should bring!

-Chris Getzlaf, Partner at CG Wealth Management

What’s New

When this month’s newsletter was being drafted, various monumental global events, primarily regarding the international trade war, occurred in a short amount of time. As of yesterday (April 9), the US administration has announced that there will be a 90 day pause on all the reciprocal tariffs that were initially announced on April 2, 2025, aka Liberation Day, for most countries. The US government cites that a reason for this 90-day pause is that over 70 countries and counting have indicated their willingness to negotiate new international trade deals with the States. During this 90 day pause, only a 10% import tariff will be applied. At this time, it is unclear which countries will receive this pause/reduction in reciprocal tariffs. Additionally, the US Administration announced that import tariffs on Chinese goods will increase to 125% because of China’s retaliatory 84% tariff increase on US goods– up from 34% initially, beginning today (April 10).

Shifting the focus back to Canada, the CRA has announced that the new effective date for the increase to the Capital Gains inclusion rate is January 1, 2026. With this new effective date, the inclusion rate on capital gains in excess of $250,000 for individuals and all capital gains realized by corporations will increase from 50% to 66%.Therefore, if any of our clients are thinking about taking on a larger capital gain as described previously, give the office a call to chat with Chris to talk potential strategies that you might want to consider.

Market Updates

The top headlines in the market in March were:

Equity markets globally were down in March. In Canada, the S&P/TSX was down over -5% and in the States, the S&P 500 was down over -6%. Looking to broader international markets, like Asia, the Nikkei 225 was down a little over -4%. The pullbacks we saw in March were in relation to the uncertainty for investors as April 2, the date that the USA planned to announce global reciprocal tariffs against various countries, neared.

Due to the uncertainty flooding the markets near the end of March, gold reached a record high spot price of over $3,100 USD per ounce. Historically, gold has been known as a “safe haven” for investors and can increase in price during times of volatility.

Numerous mega-giant giant companies have announced major investment plans into the US over the next several years:

Apple announced a $500 billion investment in the US over the next four years.

Nvidia and TSMC, two of the world leaders in chip manufacturing that supports artificial intelligence plan to invest hundreds of billions of dollars in the US over the next four years.

Johnson& Johnson announced their plan to increase US investment to more than $55 billion over the next four years

Macroeconomic Updates

The top headlines in the macroeconomic sphere in March were:

The Bank of Canada further reduced the interest rate by 0.25% to 2.75%, the lowest level since September 2022. This marks the seventh consecutive cut in interest rates in Canada. The next rate decision is on April 16

In March, Statistics Canada released February’s inflation numbers. In Canada, inflation grew at the fastest pace in eight months as the Consumer Price Index rose at a 2.6% yearly pace, the highest rate since June and up from 1.9% in January.

Despite the whirl wind tariff talk that has flooded the news since the beginning of April, as a recap, these were the top tariff headlines in March.

China placed a 100% import tariff on Canadian Canola, as well as other agri-food products, in response to the Canadian Federal Government’s 100% import tariff on Chinese-made electric vehicles.

On March 4,US tariffs of 25 per cent on Canadian goods and 10 per cent on energy and potash exports from Canada came into effect.

On March 12, the US imposed tariffs of 25% per cent on Canadian steel and aluminum products

Mark Carney won the Liberal Leadership race on March 9, as he secured more than 85% of the Liberal Party’s vote. Nearly a week later, on March 14, Justin Trudeau officially resigned as Prime Minister of Canada and Mark Carney was sworn into office. Carney’s most notable actions taken as the new Prime Minister thus far have been:

Called a federal election to occur on April 28, 2025.

Reduced the consumer carbon tax to $0. Despite the Prime Ministers reduction in the carbon tax, he has not scrapped the underlying legislation that enabled the Federal government to levy the tax in the first place. This means that, in theory, that the consumer carbon tax could be increased in the future.

The Saskatchewan Provincial Government tabled the 2025-26 provincial budget on March 19. Some highlights from the budget include:

Taxation changes provide over $250 million in tax savings this year for Saskatchewan residents ,in addition to the more than $2 billion in affordability measures in every budget.

Funding to operate Saskatchewan kindergarten to grade 12 schools will increase by $186 million, or8.4 per cent, for a total of $2.4 billion for the 2025-26 school year.

Provincial health care funding will increase by $485 million, or 6.4 per cent, over the previous year for a record total $8.1 billion for the year.

Please don't hesitate to contact us if you have any questions. The team is looking forward to helping you plan to prosper.

CG Wealth Management March Newsletter

As we turn the page on February and the bitter cold it brought to Saskatchewan, I wanted to send a couple of reminders as we start income tax season.

Personal Note From Chris Getzlaf

As we turn the page on February and the bitter cold it brought to Saskatchewan, I wanted to send a couple of reminders as we start income tax season.

March 3rd was the last day to contribute to your RRSP or a Spousal RRSP and receive the tax deduction for the 2024 tax year.

Investment companies and employers had until the end of February to send out their investment tax slips for registered accounts (RRSP, RIF, FHSA, etc.) and T4s. So, if you were expecting any of these slips in the mail, you may have to wait a few more business days before receiving them.

Investment companies have until the end of March to send out their investment tax slips for non-registered accounts.

If you are interested in having your tax returns completed by Glen Koshman, as noted in last month’s newsletter, please let me know and we will be happy to send you instructions on when and where to submit your income tax information.

Enjoy this month’s edition of our newsletter and be sure to take advantage of the nicer spring weather that we should experience this March!

-Chris Getzlaf, Partner at CG Wealth Management

Market Updates

The top headlines in the financial markets in February were:

The main markets were slightly down on the month, despite posting all time highs mid-month. The S&P/TSX, the was slightly down -0.44% and the S&P was down -1.31%.

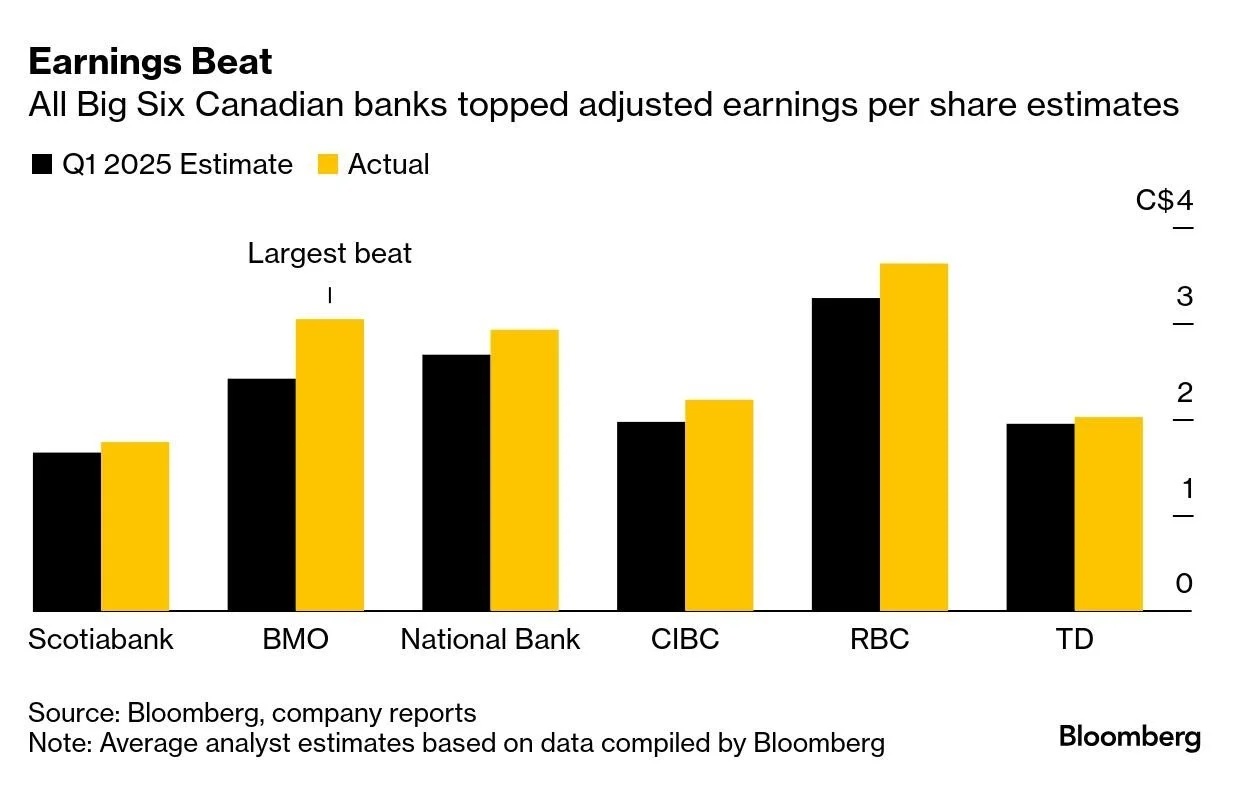

All major six banks in Canada reported earnings in the last week in February. Every single one of them topped analyst expectations for earnings.

Macroeconomic Updates

The top headlines in the broader macroeconomy that we paid attention to in January were:

The Consumer Price Index (CPI), aka inflation, rose 1.9% year-over-year in January, following an increase of 1.8% in December, staying at or below the Bank of Canada’s 2% target for a sixth straight month.

The central bank next sets the benchmark overnight rate on March 12. Economists are split into two camps, with one expecting the bank to keep cutting rates and other seeing it pausing amid rising uncertainties.

U.S. tariffs on Canadian exports were paused for the month of February. On March 4, 2025, U.S. tariffs of 25 per cent on Canadian goods, and 10 per cent on energy exports from Canada imported into the U.S. from Canada, came into effect. The U.S. has indicated that this action is in response to national security concerns, particularly related to illegal immigration and the flow of fentanyl and other drugs into the U.S.

In response to the State’s tariffs, the Canadian government announced it’s first set of countermeasures, which included imposing tariffs on $30 billion in goods imported from the States.

The U.S. has also announced that it may impose additional 25 per cent tariffs on certain industries, including steel, aluminum and autos on March 12.

If you enjoyed the newsletter and want to start receiving them as a client, please reach out to use below!

CG Wealth Management February Newsletter

As we close out the first month of 2025, it feels like a year’s worth of news and global events have already happened – the announcement of the Prime Minister’s intended resignation, wildfires that decimated parts of southern California, the inauguration of the 47th President of the USA, and a cease-fire in the middle east are just to name a few…

Personal Note From Chris Getzlaf

As we close out the first month of 2025, it feels like a year’s worth of news and global events have already happened – the announcement of the Prime Minister’s intended resignation, wildfires that decimated parts of southern California, the inauguration of the 47th President of the USA, and a cease-fire in the middle east are just to name a few…

With the speed which these global events seem to be occurring and their contribution to the uncertainty in the market, I believe it is the right time to speak a bit about the market volatility we have been experiencing in the last month.

If there is one thing to take away from this edition of the newsletter, it is that wealth accumulation isn’t always a smooth climb. From time to time, the market will experience some turbulence, it is inevitable.

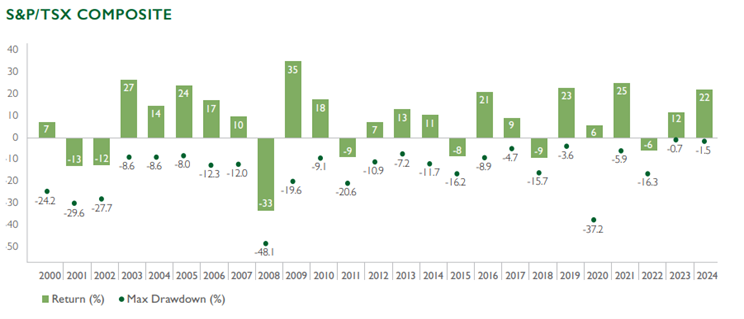

Just take the below graph as an example. Since the turn of the millennium, 14 out of 25 years experienced drawdowns of 10% or greater, BUT only seven of those years ended in negative territory.

Even if we look at this past January, the S&P/TSX’s worst day was down 1.22%. Fast forward to the end of the month, and we finished the month up overall nearly 3.3%!

It’s during these times of volatility that good opportunities to invest in the market arise.

Remember, wealth accumulation takes time and isn’t always a smooth ride.

-Chris Getzlaf, Partner at CG Wealth Management

What’s New

As a valued client of CG Wealth Management, we want to remind you that we offer tax preparation, filing, and mock return services. As the 2024 tax filing season starts to ramp up, here is what you need to know and start preparing for:

1) Key dates this tax season are:

March 3, 2025: The last day to contribute to your RRSP or a Spousal RRSP and receive the tax deduction for the 2024 tax year. If you’re interested in topping up either, if eligible, please reach out to our office and Chris would be happy to work with you.

April 30, 2025: The last day to file for most individuals.

June 16, 2025: The last day to file for self-employed individuals.

2) Despite Glen Koshman’s retirement from providing financial advisement services, he will still be preparing and filing income tax returns for CG Wealth Clients.

3) We will send out communication via email next week to clients who have regularly used this service in the past, instructing on where and how to submit your tax documents.

4) If you’re reading this, have not utilized this service before, and are interested in doing so, give our office a call or send us an email and we would be happy to forward you the instructions mentioned above once they’re finalized.

5) Employers and Investment companies have:

Until the end of February to send out their investment tax slips for T4s and registered accounts (RRSP, RIF, FHSA, etc.).

Until the end of March to send out their investment tax slips for non-registered accounts.

Market Updates

The top headlines in the financial markets that we paid attention to in January were:

The S&P/TSX was up nearly 3.3% in January whereas in the U.S., the S&P 500 reported a 2.7% gain.

A tit-for-tat tariff fight among the world’s major economies adds fresh headwinds to the outlook for global growth, for profits of companies suddenly facing higher import taxes, and for financial markets adjusting to new trade flows.

Global financial markets were shaken by news of afresh artificial intelligence model from Chinese startup DeepSeek, which raised questions over America’s technological dominance and fueled concerns that high U.S. tech valuations may come under pressure. The latest AI model of DeepSeek, released last week, is widely seen as competitive with those of Open AI and Meta Platforms Inc.

Macroeconomic Updates

The top headlines in the broader macroeconomy that we paid attention to in January were:

Starting mid-to-late January, Canada and Mexico were preparing to impose retaliatory tariffs due to the U.S.’s 25% headline tariffs on both country’s various imports. In a whirlwind 72 hours, Canada and Mexico agreed to and announced enhanced border security measures. As a result, all parties agreed to delay all proposed tariffs for approximately a month, during which time further trade negotiations are set to occur.

The Federal Government announced that they will be pushing back the implementation date for their new proposed capital gains tax. The new effective date is now January 1, 2026.

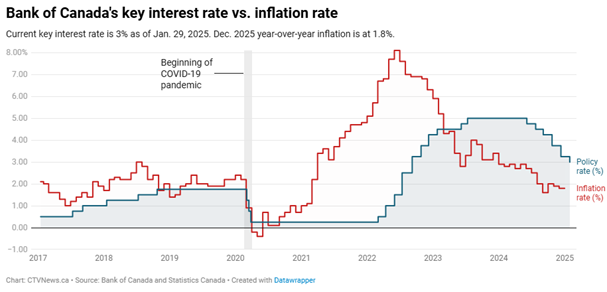

On January 29, 2025, the Bank of Canada further reduced the overnight rate by 0.25%, resulting in the target overnight rate being 3.00%. This was the Bank of Canada’s sixth consecutive rate cut since June of 2024. The next interest rate decision is March 12, 2025. Below is a graph that shows Canada’s inflation rate vs interest rate.

Statistics Canada reported on January 21st that the national annual inflation rate was 1.8% in December. The month over month decrease was partly attributed to the federal government’s temporary GST/HST tax break.

Donald Trump was inaugurated as the 47th President of the United States of America on January 20, 2025.

A total of six Liberal leadership contenders have emerged since the Prime Ministers resignation announcement. The two individuals who appear to be leading the Leadership race currently are former central banker Mark Carney, and former Finance Minister and current MP, Chrystia Freeland.

What is a Tariff? What is all the Fuss About?

As the talk of tariffs and a potential tariff war flooded the news cycle in January, we thought it would be good to give a quick briefer for everything tariffs.

What is a tariff?

A tariff is a tax put on an imported good(s) by a government.

How do they work?

When a tariff is applied on an imported good, businesses who import that good must pay the price of the good plus the new tax(tariff) to the government.

Typically, that business who imports that good will then raise their prices so that their new costs are covered, essentially passing the majority of the burden onto the consumer.

Why use tariffs?

Tariffs are meant to make foreign imported goods more expensive, incentivizing you to buy that same good from a local business.

Who do tariffs Impact?

Broadly speaking, tariffs affect:

You: The increase in cost of the good maybe passed onto you by the business as they may increase their prices.

Local Businesses: Local businesses who make the same tariffed good for the same price or cheaper may benefit as consumers will opt to buy something that is cheaper and local.

Foreign Government & Businesses: Foreign businesses and governments may be hurt or benefit financially from tariffs depending on the amount of goods imported/exported.

In conclusion, tariffs can be a doubled edged sword. While they can increase costs for you, the consumer, they can also protect and support local businesses and economies.

If you have questions about how tariffs are affecting your portfolio or how you can mitigate tariff risk. Please reach out, we would be happy to further discuss!

CG Wealth Management January Newsletter

Happy New Year! I hope you had a great holiday season with friends and family and were able to take some time to rest and recharge before the new year! As of January 2nd, our office doors have reopened, and the team is excited and ready for a great 2025!

Personal Note From Chris Getzlaf

To all CG Wealth Management clients, Happy New Year! I hope you had a great holiday season with friends and family and were able to take some time to rest and recharge before the new year! As of January 2nd, our office doors have reopened, and the team is excited and ready for a great 2025!

The CRA has announced that the TFSA contribution limit for 2025 is $7,000. If you haven’t already been contacted by me to contribute to your TFSA, feel free to reach out if you want to get your TFSA topped up, or have any questions about this year’s limit.

With the new year, comes new resolutions. If one of your new resolutions includes your finances, like you’re planning on retiring this year, want to create a budget that reduces your debt but also invests for the future, or want to get into a better habit of saving and investing regularly, as a CG Wealth Client, our team would be happy to work towards those types of resolutions with you.

Before getting to the bulk of the newsletter, I wanted to let you know that the office has a Facebook page where we post regular updates. So, if you haven’t already done so, click the button below and give us a follow!

To all our clients, have a great start to the new year!

-Chris Getzlaf, Partner at CG Wealth Management

What’s New

Typically, our newsletter focuses on the major events that happened the month prior, however, we would be remiss if we didn’t acknowledge that Prime Minister Justin Trudeau officially announced his intent to resign as Prime Minister and the leader of the Liberal Party on January 6, 2025. At the same time, the Prime Minister confirmed that Parliament has been prorogued (suspended) until March 24, 2025.

Of the various impacts this will have, there is a possibility that the proposed changes to the capital gains tax as announced in the 2024-25 federal budget could become void due to how the proposed changes were introduced in Parliament.

The team will continue to monitor the situation as it progresses.

As a refresher, in its 2024-2025 budget, the federal government had announced that it was increasing the Capital Gains Inclusion Rate to 66 2/3%, on all gains earned by corporations and trusts, and on gains realized by individuals annually over $250,000, effective June 25, 2024.

Market Updates

The top headlines in the financial markets that we paid attention to in December were:

In Canada, the S&P/TSX recorded its best year since 2021, gaining over 21% in total return. After getting off to a slow start, the TSX gained speed after the Bank of Canada began its rate-cutting cycle in June.

In the U.S., the S&P 500, which set 57 record highs in 2024, finished up about 23% for the year in USD terms and more than 36% in CAD.

The tech-heavy Nasdaq was up 29% in USD.

Markets got a massive boost in 2024 from investor enthusiasm around artificial intelligence. Stocks with exposure to the AI business, such as Nvidia, saw their prices increase greatly. It remains to be seen whether those gains can be maintained in 2025.

Macroeconomic Updates

The top headlines in the broader macroeconomy that we paid attention to in December were:

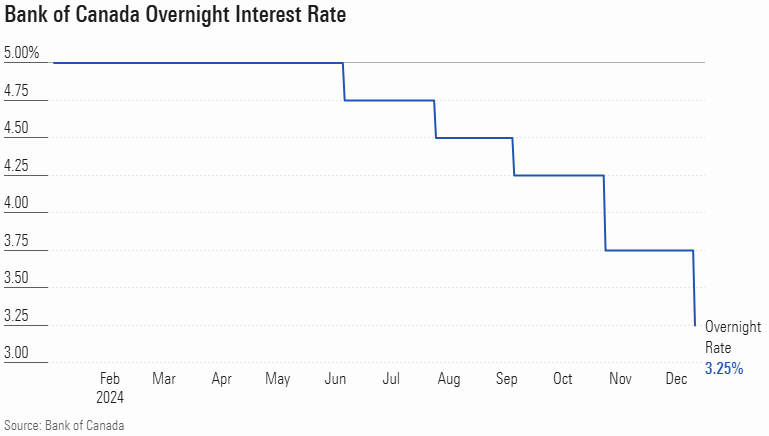

On December 11, 2024, the Bank of Canada cut the overnight rate by 0.50%, resulting in the target overnight rate being 3.25%.This was the Bank of Canada’s fifth consecutive rate cut since it’s first in June of 2024 (see chart below).

According to Statistics Canada, the most recent Consumer Price Index was 1.9% in November, down from a 2.0% increase in October. Slower price growth was broad-based, with prices for travel tours and the mortgage interest cost index contributing the most to the deceleration.

On December 16th, the Federal Government of Canada released its 2024 Fall Economic Statement, which outlines their economic plan for the year. Of the 279 page document, much attention was focused on the federal deficit ballooning to nearly $62 billion for the 2023-24 fiscal year.

A catalyst leading to the Prime Minister’s resignation announcement on January 6 was the unexpected resignation of Finance Minister, Chrystia Freeland, from her cabinet position, just hours before the release of the 2024 Fall Economic Statement. Her resignation marked the fifth cabinet Minister to step down in 2024.

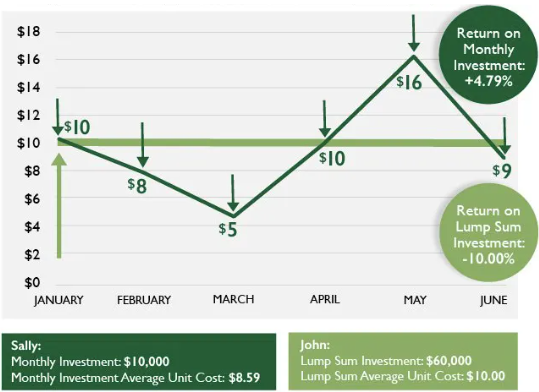

Dollar Cost Averaging - Why You Should Consider Utilizing It

A regular section of this monthly newsletter that our readers can come to expect is a “Learn” section. This section is intended to provide you with practical financial information and concepts that will help you develop your learning and understanding of the world of finance.

In this edition, we will focus on Dollar Cost Averaging, which is an effective way to invest your money. Here is how it works:

Instead of investing your money all at once, you can dollar cost average and invest smaller amounts at regular times, like weekly, bi-weekly, or monthly. This means that when the price of shares are low, you buy more shares, and when they’re high, you buy fewer. The benefit of dollar cost averaging is that it:

Provides consistency as your overall returns will reflect the general trend in the investment’s performance, rather than the specific price from one day.

Reduces risk as it protects you from significant draw downs if you were to potentially buy only at the peak of the market.

Encourages consistent saving and investing as the strategy requires you save money and invest the savings regularly.

The most effective way to start dollar cost averaging is to set up a regular contribution plan to one or more of your plans, like a TFSA, Non-Registered account, or RRSP. What many like to do is set up a contribution plan that coincides with their pay period so that a portion of their pay cheque is automatically saved and invested – out of sight, out of mind.

Remember it’s about time in the market, not timing the market!

To illustrate the benefits of dollar cost averaging, consider the example below.

If you do not already have a systematic contribution plan on one or more of your plans and want to take advantage of this effective investing strategy, please reach out to myself and I’d be happy to help you create a strategy that works for you!